With inflation on the rise, many investors are wondering what to invest in to beat inflation and protect their savings. As the old saying goes, inflation is taxation without legislation – it erodes the purchasing power of your money over time. So how can savvy investors aim to mitigate inflation risk? Here are some tips from the alternative investment firm New Capital Link.

Inflation reared its ugly head in 2021 after years of muted price rises, climbing to highs not seen in decades. With inflation expected to remain elevated in 2022, investors need to take action to beat inflation with their portfolios. The good news is that while inflation can seem daunting, there are tried and true ways to aim to keep your money working as hard as you did to earn it.

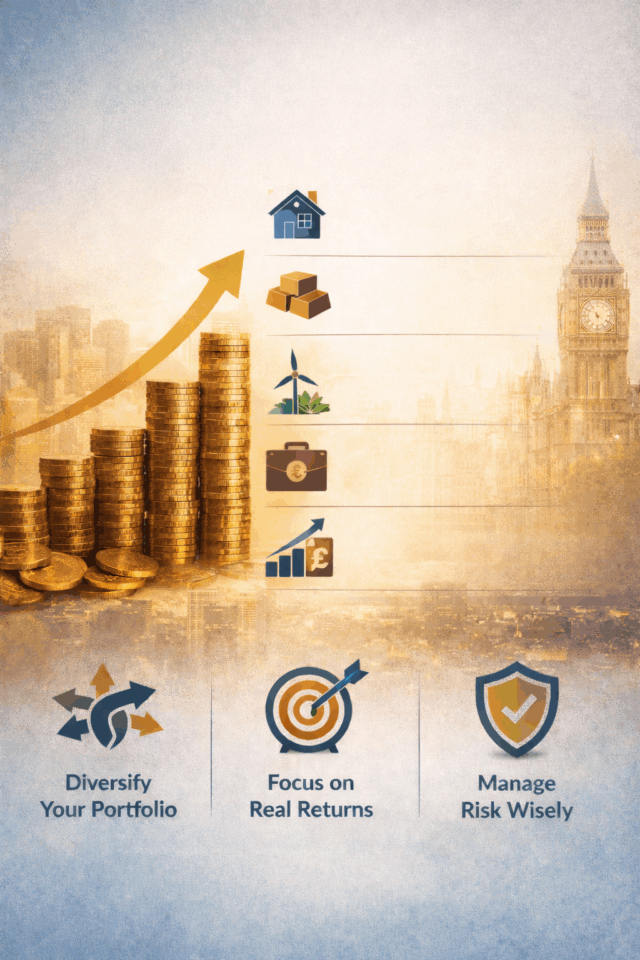

Diversify Across Asset Classes

One of the best defences is to diversify your portfolio across different asset classes. Stocks, bonds, real estate, commodities, and alternative investments like private equity can all have a role to play. Each asset class has differing sensitivities to inflation, so blending them can aim to smooth out inflationary impacts. Within each asset class, further diversification is key — such as holding domestic and international stocks across different sectors.

Focus on Real Assets

Real assets are those with inherent worth due to their tangible value, such as real estate, commodities, or infrastructure. As inflation rises, the price of real assets also tends to rise. This helps mitigate inflation risk relative to paper assets like stocks and bonds. Some examples of real asset investments include real estate investment trusts (REITs), energy pipelines, timberlands, farmlands, and commodities funds.

Consider TIPS

Treasury Inflation-Protected Securities (TIPS) are government bonds whose principal value rises with inflation. So as consumer prices increase, TIPS are designed to have their face value and interest payments adjust higher. This feature aims to preserve the purchasing power of the investment. While returns can be more muted than stocks, TIPS provide steady income and inflation protection.

Embrace Equities

Equities have been proven inflation fighters over long periods thanks to their growth potential. Companies tend to increase product prices as their input costs rise, aiming to at least keep up with inflationary pressures. Rising dividends over time can also help mitigate inflation impacts for investors focused on income strategies. Equities do come with higher short-term volatility though — a risk some investors may want to offset via asset class diversification.

The Risks of Cash

Conversely, cash is one of the asset classes most vulnerable to inflation erosion. Savings account interest rates may creep higher as central banks raise rates, but likely not enough to outpace inflation. As the purchasing power of money held in cash decreases yearly, investors risk not keeping up with inflation or reaching their financial goals.

Inflation-Beating Alternative Investments

As discussed above, diversification and real assets are two keys to crafting an inflation-resistant portfolio. At London-based alternative investment firm New Capital Link, their specialised investment products open up new opportunities in these areas for accredited investors. With over 5 years of proven returns, New Capital Link has established partnerships globally to deliver custom alternative investment solutions.

Areas they focus on include real estate, venture capital in growth sectors like fintech, as well as fund of funds structures. These strategies are designed to generate returns less correlated to traditional holdings while providing specialised exposures harder to access for everyday investors. Many target between 10-15% yearly returns over the longer term – well above inflation.

In today’s uncharted monetary environment with higher inflation risks, New Capital Link builds portfolios aiming to mitigate downside risks through expanded diversification. At the same time, they pursue upside opportunities by tapping into specialised assets with return profiles not always accessible to traditional equity and bond investors.

Inflation may be top of mind today for many investors but know that there are time-tested strategies to aim to beat it over time. Inflation can be a good thing, encouraging economic growth and carefully positioned investment portfolios. By diversifying into real assets and considering vehicles like private equity, investors can take proactive steps to strive for healthy returns even with rising inflation.