Receiving an inheritance can be both a blessing and a challenge. While it provides financial opportunities, it also comes with managing and investing this newfound wealth wisely. This guide will walk you through the essential considerations and strategies for investing your inheritance, helping you make informed decisions that can secure your financial future.

Things to ask yourself

Before diving into investment strategies, taking a step back and evaluating your current financial situation and goals is crucial. Here are some key questions to consider:

- What are my immediate financial needs?

- Do I have any outstanding debts to pay off?

- What are my long-term financial goals?

- How much risk am I comfortable taking?

- Do I need professional financial advice?

Answering these questions will help you create a solid foundation for your investment strategy.

Can your inheritance work harder for you?

Many people wonder if they can make their inheritance grow through smart investments. The answer is often yes, but it requires careful planning and consideration.

Alex Santos, an alternative investment introducer, offers this perspective: “Investing an inheritance can be a powerful way to build long-term wealth. However, it’s important to approach this opportunity with a clear strategy and an understanding of your risk tolerance. Don’t rush into decisions – take the time to educate yourself and consider seeking professional advice to maximise the potential of your inheritance.”

By exploring various investment options and aligning them with your financial goals, you can potentially make your inheritance work harder for you, generating returns that can support your future financial needs.

The types of inheritance

Inheritances can come in various forms, each with its own considerations for investment:

Stocks and shares

Stocks and shares offer the potential for high returns but come with higher risk. In recent years, we’ve seen increased retail investor participation through user-friendly apps like Robinhood and eToro. The S&P 500, a key benchmark for stock performance, has shown an average annual return of about 10% over the long term, although past performance doesn’t guarantee future results. It’s worth noting the rise of ESG (Environmental, Social, and Governance) investing, which allows investors to align their portfolios with their values.

Bonds

Bonds are generally lower risk but also offer lower returns compared to stocks. In the current low-interest-rate environment, bond yields have been historically low. However, they still play a crucial role in portfolio diversification. Corporate bonds, government bonds (like US Treasuries or UK Gilts), and municipal bonds are common options. The emergence of green bonds, which fund environmentally friendly projects, has been a notable trend in recent years.

Mutual funds and ETFs

Mutual funds and ETFs (Exchange-Traded Funds) provide diversification and professional management. ETFs, in particular, have gained popularity due to their lower fees and intraday trading capability. According to Statista, the global ETF market reached $7.74 trillion in assets under management by the end of 2020. Thematic ETFs, focusing on specific trends like artificial intelligence or clean energy, have become increasingly popular among investors looking to capitalise on long-term trends.

Real estate

Real estate can offer both rental income and potential appreciation. The rise of REITs (Real Estate Investment Trusts) and crowdfunding platforms has made real estate investing more accessible. In the UK, the average house price increased by 10.2% in the year to March 2021, according to the Office for National Statistics. However, real estate markets can vary significantly by location, and it’s important to consider factors like property management and liquidity.

Savings accounts and CDs

Savings accounts and CDs (Certificates of Deposit) offer low risk but also low returns in the current interest rate environment. As of 2021, interest rates remain at historic lows in many countries. However, some online banks and fintech companies offer higher-yield savings accounts that can provide slightly better returns than traditional banks. It’s worth shopping around and comparing rates.

Retirement accounts

Retirement accounts can offer tax advantages for long-term savings. In the UK, options include personal pensions, SIPPs (Self-Invested Personal Pensions), and workplace pensions. The annual allowance for pension contributions is £40,000 for most people (as of 2021/2022 tax year), but this can be lower for high earners or those who have already started drawing from their pension.

Education savings plans

Education savings plans are beneficial if you have children or grandchildren to support. In the UK, Junior ISAs (Individual Savings Accounts) allow you to save up to £9,000 per child per year (2021/2022 tax year) tax-free. In the US, 529 plans offer tax-advantaged savings for education expenses. With the rising cost of education globally, these plans can provide a valuable head start for young family members.

Start a business

For those with entrepreneurial ambitions, using an inheritance to start a business can be a path to long-term wealth creation. The COVID-19 pandemic has accelerated digital transformation, creating new opportunities in e-commerce, remote services, and health tech. However, starting a business comes with significant risks and requires careful planning and often expertise in the chosen field.

Peer-to-peer lending

Peer-to-peer lending is a newer form of investment with potential for higher returns. Platforms like Zopa in the UK or Prosper in the US connect borrowers directly with lenders, often offering higher interest rates than traditional savings accounts. However, it’s important to note that these investments come with higher risk and less regulatory protection compared to traditional banking products.

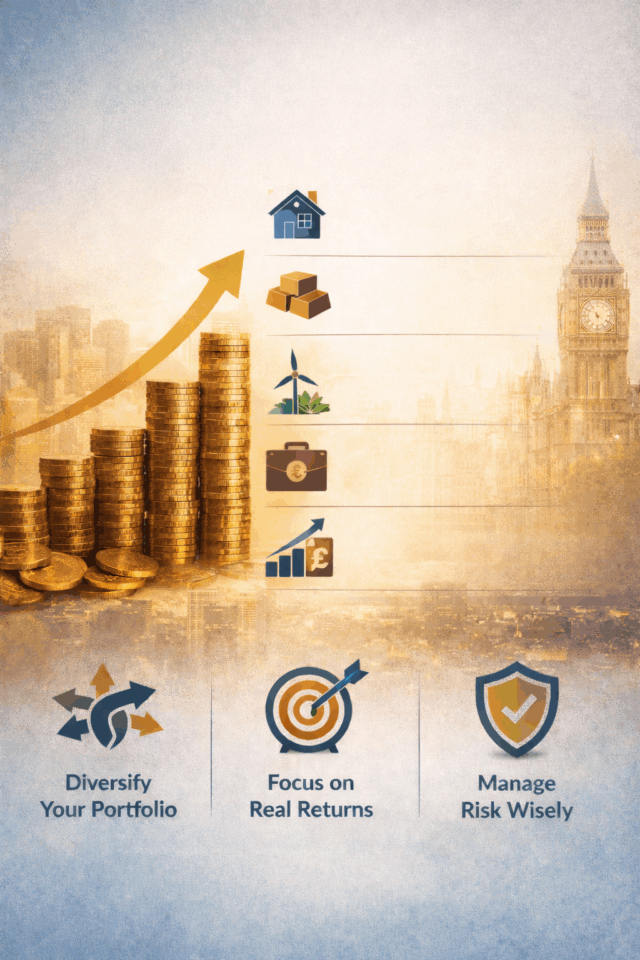

When deciding how to invest your inheritance, it’s crucial to consider your financial goals, risk tolerance, and time horizon. Diversification across different types of investments can help manage risk. As always, it’s advisable to consult with a financial professional to create an investment strategy tailored to your individual circumstances.

Understanding the type of inheritance you’ve received is crucial in determining the best investment approach.

How does inheritance tax work on investments?

Inheritance tax can significantly impact the amount you have available to invest. In the UK, inheritance tax rules are complex and subject to change. Here are some key points to consider:

- There’s usually no inheritance tax to pay if the value of the estate is below £325,000.

- The standard inheritance tax rate is 40% on anything above the £325,000 threshold.

- There are various exemptions and reliefs available, such as the residence nil-rate band for property.

- Certain investments, like those in qualifying businesses, may be eligible for Business Property Relief, potentially reducing the inheritance tax burden.

It’s advisable to consult with a tax professional to understand how inheritance tax might affect your specific situation and investment choices.

What are the different investments inheritance can be used for?

When it comes to investing your inheritance, you have a wide array of options. Here are some common investment vehicles to consider:

- Stocks and shares: Offer potential for high returns but come with higher risk.

- Bonds: Generally lower risk but also lower returns compared to stocks.

- Mutual funds and ETFs: Provide diversification and professional management.

- Real estate: Can offer both rental income and potential appreciation.

- Savings accounts and CDs: Low risk but also low returns in the current interest rate environment.

- Retirement accounts: Can offer tax advantages for long-term savings.

- Education savings plans: If you have children or grandchildren to support.

- Start a business: For those with entrepreneurial ambitions.

- Peer-to-peer lending: A newer form of investment with potential for higher returns.

The right mix of investments will depend on your financial goals, risk tolerance, and time horizon.

Are alternative investments suitable for inheritance investing?

Alternative investments can play a role in a diversified investment strategy, but they require careful consideration. These investments typically include:

- Private equity

- Hedge funds

- Commodities

- Cryptocurrencies

- Collectibles (art, wine, etc.)

- Structured products

Alex Santos weighs in on this topic: “Alternative investments can offer diversification benefits and potentially higher returns compared to traditional investments. However, they often come with higher risks, less liquidity, and more complexity. For those investing an inheritance, alternative investments should generally make up only a small portion of a well-diversified portfolio, if at all. It’s crucial to thoroughly understand these investments and consult with a financial advisor before committing funds.”

Alternative Investments London

New Capital Link, based in London, specialises in introducing investors to alternative investment opportunities. With a deep understanding of the London investment landscape, New Capital Link helps clients navigate the complex world of alternative investments.

Our team of experienced professionals works closely with investors to understand their financial goals and risk tolerance. We provide access to a curated selection of alternative investment opportunities, ranging from real estate developments to private equity deals in the thriving London market.

At New Capital Link, we believe in empowering our clients with knowledge and opportunities. Whether you’re looking to diversify your inheritance investments or explore new avenues for wealth creation, our experts are here to guide you through the process.

Remember, while alternative investments can offer exciting opportunities, they should be approached with caution and as part of a balanced investment strategy. Always conduct thorough research and seek professional advice before making investment decisions.

Investing an inheritance is a significant responsibility that can have long-lasting implications for your financial future. By carefully considering your options, understanding the tax implications, and potentially seeking professional advice, you can make informed decisions that align with your financial goals and risk tolerance. Whether you choose traditional investment vehicles or explore alternative options, the key is to approach the process thoughtfully and with a clear strategy in mind.